The non-QM market is no longer a niche — it’s becoming a core part of how brokers do business. Non-QM originations surpassed $120 billion in 2025, far exceeding early projections, and industry analysts forecast the segment could reach $150–$180 billion in 2026 depending on rate movement (Mortgage Professional America). For brokers still operating exclusively within agency guidelines, that’s a significant opportunity going unserved.

At LendSure Mortgage Corp., we’ve built our entire platform around exactly this borrower base — creditworthy clients whose financial profiles simply don’t fit the conventional box. Understanding what non-QM requires, who it serves, and how it works in 2026 is the foundation of a more resilient, diversified broker business.

Why Non-QM Exists: The Regulatory Foundation

Non-QM lending didn’t emerge as a workaround — it emerged as a necessary solution within a clearly defined regulatory framework. The CFPB’s Ability-to-Repay/Qualified Mortgage rule established strict standards for what constitutes a Qualified Mortgage (QM) under the Truth in Lending Act. Loans that don’t meet those standards — due to documentation type, income structure, or product features — fall outside the QM category.

Critically, non-QM loans are not exempt from ATR obligations. As the CFPB confirms, all mortgages must demonstrate the borrower’s ability to repay — non-QM simply does so through alternative documentation rather than standard W-2 and tax return verification. That distinction is important: non-QM is not subprime. It’s a different documentation pathway for creditworthy borrowers.

What QM Doesn’t Allow — And Why That Matters

The official QM definition under Regulation Z places limits on loan features, points and fees, and certain income verification methods. Non-QM lending exists in the space where those restrictions create gaps — for self-employed borrowers, real estate investors, and high-net-worth individuals whose finances are real but whose documentation doesn’t follow a W-2 template.

The FDIC has confirmed that offering non-QM loans is not inherently unsafe, provided underwriting and risk management remain prudent. In fact, the average FICO score of non-QM borrowers in 2024 was 776 — comparable to conventional mortgage borrowers — demonstrating that alternative documentation does not equate to elevated credit risk.

The 2026 Regulatory Landscape

Brokers expanding into non-QM in 2026 should be aware of updated compliance thresholds that affect how certain loans are classified and originated. The CFPB’s annual Regulation Z threshold adjustments update APR spreads and dollar triggers that determine QM status under TILA — meaning a loan that fell outside QM parameters last year may be classified differently in 2026.

Updated appraisal thresholds for higher-priced mortgage loans also affect non-QM originations, particularly for higher-value transactions. Staying current on these broader consumer law changes effective in 2026 helps brokers advise clients accurately and avoid compliance surprises at closing.

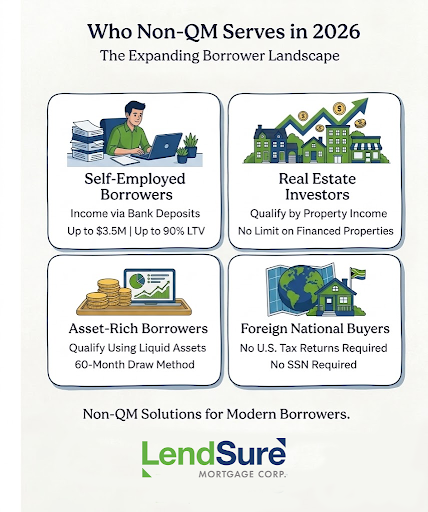

Who Non-QM Serves in 2026

The non-QM borrower base has expanded significantly — and understanding who these clients are is the first step to recognizing them in your pipeline.

Self-employed individuals remain the largest segment. With approximately one in ten working adults now classified as self-employed, many have strong cash flow but can’t document income through traditional tax returns. Our Bank Statement Mortgage program qualifies these borrowers on 12 or 24 months of deposits, with loan amounts up to $3.5M and LTV up to 90%.

Real Estate Investors

Investor purchase share is expected to remain above 25% in 2026 and 2027, according to Cotality — driven by affordability constraints that continue to favor cash-flowing rental properties over primary home purchases. Our DSCR Expanded Investor program qualifies investors on property income rather than personal financials, with no limit on financed properties and loan amounts up to $3M.

High-Net-Worth and Foreign National Borrowers

Asset-rich borrowers who don’t show traditional monthly income — retirees, trust beneficiaries, and those transitioning between employment — may qualify through our Asset Depletion / Asset Qualifier program using liquid assets over a 60-month draw period. Our Foreign National program serves international investors with no U.S. tax returns, SSN, or domestic credit history required.

Core Non-QM Documentation Types

One of the most practical questions brokers ask is: what does non-QM actually require? The answer depends on the borrower profile, but the most common documentation pathways are well established.

- Bank Statement loans use 12 or 24 months of personal or business deposits to calculate qualifying income — no tax returns required.

- DSCR loans require no personal income documentation at all; approval is based on the property’s debt service coverage ratio.

- Asset Qualifier loans use verified liquid assets divided over a draw period to establish qualifying income.

- P&L loans qualify self-employed borrowers on a CPA-prepared profit and loss statement with minimal bank statement support.

What Non-QM Lenders Look For

Despite the flexibility in documentation, non-QM lenders still underwrite thoroughly. Property value, collateral quality, borrower credit profile, and a clear repayment capacity remain central to every approval. Our pre-underwriting process provides common-sense approvals within 24 hours — giving brokers fast, reliable feedback before investing time in full documentation.

Submit your scenario to see how we’d approach your client’s file.

Why Non-QM Deals Fall Apart — and How to Prevent It

Even well-qualified non-QM borrowers can hit unexpected roadblocks when files aren’t structured correctly from the start. Understanding the most common deal-killers helps brokers prepare cleaner submissions and protect their clients’ timelines.

The most frequent issue is documentation gaps. Bank statement files fall apart when deposits are inconsistent, large non-payroll deposits go unexplained, or the borrower has recently switched from personal to business accounts mid-period. Preparing borrowers for what lenders will scrutinize — and gathering documentation early — prevents last-minute surprises.

Mismatched Program Selection

Selecting the wrong program for a borrower’s actual income structure is another avoidable source of deal failure. A self-employed borrower with strong bank deposits but a weak P&L — or vice versa — may qualify cleanly under one program and poorly under another. Taking time upfront to match the borrower’s documentation strength to the right product makes a measurable difference in approval outcomes.

Property eligibility is a third common friction point, particularly for investors. Non-warrantable condos, condotels, and properties with commercial space require additional building documentation that, when missing, can stall a file well into processing. Ordering a Condo Questionnaire early and confirming property eligibility before full submission keeps deals on track.

The Business Case for Brokers

The market data makes a compelling case. Non-QM grew from less than 3% of U.S. mortgages in 2020 to 8% by July 2025 (Scotsman Guide / Optimal Blue). According to S&P Global, non-QM loans are projected to represent nearly 30% of non-agency mortgage-backed securities — and one industry executive projects the non-agency space could account for one in four or five loans originated in 2026.

Brokers who expand into non-QM aren’t just adding products — they’re building a more resilient pipeline. Investor clients, self-employed borrowers, and foreign nationals generate repeat business and referral relationships that conventional-only brokers simply can’t cultivate.

Building the Expertise That Drives Referrals

Expertise in non-QM is itself a competitive differentiator. When a borrower is declined by a traditional lender and a broker can step in with a credible solution, that broker becomes the go-to resource for every non-standard scenario in their network.

Our broker resources hub, mortgage professional webinars, and Mastering Non-QM white paper are all designed to help brokers build that expertise efficiently. The more fluent you become in these programs, the more confidently you can serve a growing segment of the market.

Ready to Expand Your Pipeline?

Non-QM is no longer the future of mortgage lending — it’s the present. Brokers who understand the documentation pathways, the borrower profiles, and the regulatory framework are positioned to serve a growing segment of the market that conventional lenders routinely turn away.

Explore our full range of non-QM loan programs, or contact us to talk through how our programs fit your client base. Visit our broker resources hub to get started — no formal approval needed to submit a scenario.

Frequently Asked Questions

Is a non-QM loan the same as a subprime loan?

No. Non-QM refers to the documentation pathway, not the credit quality of the borrower. Non-QM borrowers had an average FICO score of 776 in 2024 — comparable to conventional mortgage borrowers. These are creditworthy clients whose income or property type simply doesn’t fit agency documentation requirements.

Do non-QM loans still require ability-to-repay analysis?

Yes. As the CFPB confirms, all mortgages — including non-QM — must comply with the Ability-to-Repay rule. Non-QM loans satisfy ATR through alternative documentation methods such as bank statements, asset verification, or property cash flow rather than W-2s and tax returns.

What are the most common non-QM programs for brokers to know in 2026?

The most widely used programs are Bank Statement loans for self-employed borrowers, DSCR loans for real estate investors, Asset Qualifier loans for high-net-worth individuals, and Foreign National programs for international buyers. Each serves a distinct borrower profile with its own documentation requirements and LTV parameters.

How do 2026 regulatory threshold changes affect non-QM originations?

The CFPB’s annual Regulation Z threshold adjustments update the APR spread and dollar triggers that determine QM status under TILA. These changes can affect whether certain loans fall inside or outside QM parameters — which is why staying current on annual threshold updates is part of sound non-QM compliance practice.

Can a borrower qualify for non-QM with recent credit events?

It depends on the program and the nature of the event. Our Expanded Approval program and Super Prime & Alt-A programs offer options for borrowers with some credit history complexity. Our Jumbo program has a 4-year seasoning period for major credit events. Submitting a scenario is the fastest way to assess eligibility.

How quickly can a non-QM loan be pre-qualified?

Our pre-underwriting process provides common-sense approvals and pricing typically within 24 hours of scenario submission. Brokers don’t need formal approval to submit — scenarios can be sent directly through our Submit Your Scenario page at any time.

What’s the difference between bank statement loans and P&L loans?

Bank Statement loans use 12 or 24 months of deposit history to calculate qualifying income. Our Profit & Loss program qualifies borrowers on a CPA-prepared P&L statement, with no bank statements required for loans up to $1M. The right choice depends on how cleanly the borrower’s income is reflected in each documentation type.