Your self-employed client has strong deposits, solid credit, and a tax return that tells none of it. Three years of legitimate write-offs have compressed their AGI to a number no conventional underwriter will touch.

You’ve seen this before. The question isn’t whether a bank statement loan can solve it—it’s which one. The choice between a 12-month and 24-month look-back window affects qualifying income, documentation burden, and whether the deal closes on your client’s timeline. Getting it right is the job.

Why Bank Statement Loans Exist (And Why the Distinction Between 12 and 24 Months Matters)

Traditional mortgage underwriting was designed around the W-2 employee. For business owners, freelancers, independent contractors, and gig workers, that framework routinely produces an incomplete and often misleading picture.

When a small business owner deducts home office expenses, vehicle depreciation, meals, and equipment, they’re doing exactly what the tax code encourages. But those same deductions shrink the AGI that underwriters use to calculate DTI ratios. A borrower earning $18,000 a month in genuine deposits might show $5,000 in net income after write-offs—disqualifying them for a mortgage their cash flow could comfortably support.

Bank statement programs solve this by replacing tax returns with your client’s actual deposit history. Rather than asking what you reported to the IRS, we ask what actually flowed through your accounts—and then apply a Self-Employment Questionnaire to evaluate actual operating costs rather than a blanket expense ratio. Our expense factors go as low as 10%, a significant advantage for service-based businesses with genuinely low overhead.

The 12-month versus 24-month question determines the window through which we view that deposit history—and different windows reveal different things.

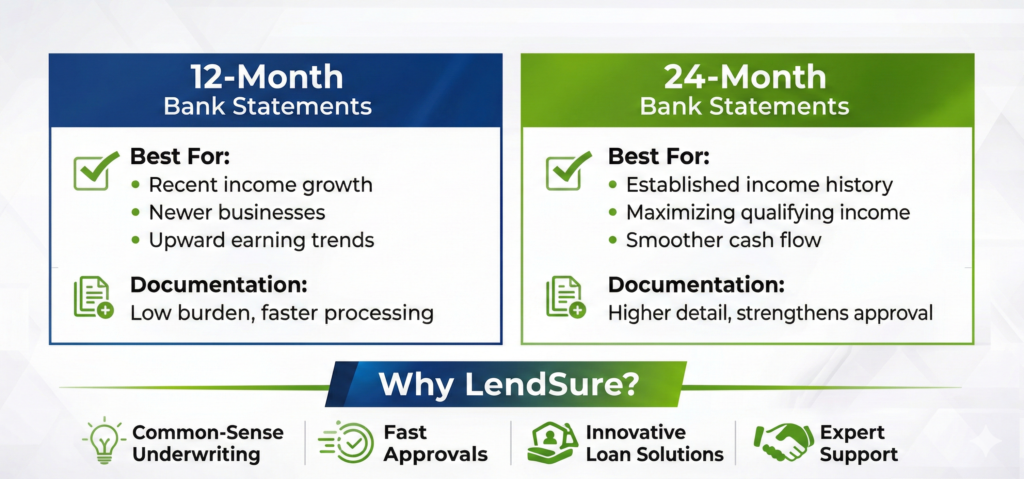

The Case for 12-Month Bank Statement Loans

A 12-month bank statement loan requires only one year of personal or business account statements to establish qualifying income. This shorter look-back period offers real strategic advantages for certain borrower profiles, and knowing when to reach for it can accelerate deals that might otherwise stall.

When a 12-Month Look-Back Works Best

Borrowers with recent income growth. A freelance designer who billed $60,000 last year but is on track for $120,000 this year has a 24-month average that significantly undersells their current capacity. A 12-month window captures the trajectory—their actual earning power today—rather than diluting it with leaner prior-year numbers. For borrowers in growth phases of their business, this isn’t just a documentation preference; it can be the difference between qualifying and not.

Newer self-employed borrowers. Not every business owner has two full years of banking history to offer. Someone who left a corporate job two years ago to launch a consulting firm may have only 14 or 16 months of meaningful deposit history as a self-employed individual. A 12-month program accommodates this reality without penalizing borrowers for the natural timeline of building a business.

Borrowers with seasonal or cyclical income patterns. In some cases, a 24-month average can be dragged down by an anomalous year—a product launch delay, a market downturn in a specific industry, or a year spent building infrastructure before revenue followed. If the prior year was an outlier and the current year demonstrates normalized or improved performance, 12 months tells the truer story.

When time is a factor. Gathering 24 months of statements across multiple accounts—including business and personal—takes time. For borrowers with purchase timelines tied to contract deadlines or competitive markets, reducing the documentation window by half can meaningfully accelerate the loan process.

The Trade-Off

A shorter look-back period introduces more volatility into income averaging. If a borrower had an unusually strong month in the prior year—a large one-time client payment, a bonus, a business sale—that single month carries more weight in a 12-month calculation than it would in a 24-month average. For borrowers with genuinely consistent income, this tends to be a non-issue. For those with spiky or irregular deposit patterns, it can cut in either direction.

Lenders offering 12-month programs may also apply slightly different scrutiny to compensating factors, since the reduced look-back provides less historical data. Strong credit, meaningful reserves, and a solid down payment help here.

The Case for 24-Month Bank Statement Loans

The 24-month option is the longer, steadier view. It smooths volatility, demonstrates established earning history, and gives underwriters greater confidence in the durability of a borrower’s income. For the right borrower profile, it’s not a burden—it’s an asset.

When a 24-Month Look-Back Works Best

Borrowers with consistent, established income. A restaurant owner who has deposited reliably for three years, a boutique owner with steady seasonal patterns, an attorney with a stable book of business—these borrowers benefit from showing consistency rather than limiting it. A 24-month window validates what they’ve been telling you: their income is reliable and predictable. That history earns underwriter confidence in a way that 12 months cannot.

Borrowers who need the strongest possible income profile. For borrowers aiming for high-end loan requests (up to $3.5M), 24 months of bank statements can improve the strength of the income calculation by showing consistency over time and reducing the impact of short-term dips. The loan amount limits are the same with 12 or 24 months—but more history can help the borrower qualify more confidently.

Borrowers with a strong prior year followed by a softer current year. Not every business trajectory is a clean upward line. A borrower who had an exceptional year followed by a more modest one may actually produce a higher qualifying income from a 24-month average than from 12 months alone. When prior-year performance is the borrower’s strength, the longer window works in their favor.

Complex income structures. When borrowers have multiple business entities, blended personal and business accounts, or income from several different sources, 24 months of history provides the full picture needed to document income comprehensively. We can combine multiple business accounts and blend W-2 income with bank statement income—and 24 months allows underwriters to see how all of those streams interact over time.

The Trade-Off

The documentation burden is real. Gathering two years of statements across multiple accounts—especially if a borrower uses separate accounts for different business entities—requires organization and time. Some borrowers will need to track down older records or work with their banks to pull historical statements in acceptable formats. Setting clear expectations early in the process prevents deal delays.

For borrowers in active income growth phases, 24 months can also dilute current earning power with historical averages that no longer reflect their business. In those cases, the 12-month option serves them better.

Program Features That Apply to Both Options

Whether your client’s situation calls for a 12-month bank statement loan or a 24-month option, several features remain consistent across our program—and they’re worth having in your toolkit when discussing scenarios with clients.

Personal and business accounts are both accepted. Clients don’t need to funnel all income through a single dedicated account. We accept statements from personal accounts, business accounts, and we can combine multiple business accounts when borrowers operate several entities or revenue streams.

W-2 and bank statement income can be blended. Borrowers who have both a salaried position and self-employment income—a consultant who also teaches adjunct at a university, for example—don’t have to choose one income type or the other. We can layer both documentation types to build the strongest possible qualifying picture.

Expense ratios as low as 10%. For borrowers in industries with genuinely low overhead—service businesses, knowledge workers, online businesses—this is a material advantage. Many lenders apply blanket expense ratios of 50% regardless of actual business costs. We assess expense ratios based on business type, which means a technology consultant with minimal overhead isn’t being penalized the same way as a contractor with a full crew and equipment.

Up to 90% LTV available. The self-employed borrower who needs flexibility on down payment isn’t automatically disqualified from meaningful financing. At up to 90% LTV, our bank statement program allows clients to preserve capital—which is often valuable for business owners who maintain working capital as a business necessity.

Loan amounts up to $3.5M. High-income self-employed borrowers are frequently purchasing higher-value properties. Our program accommodates that reality rather than capping out where their needs begin.

A Framework for Matching Clients to the Right Option

Use this as a starting point when you’re evaluating which bank statement option fits a given scenario:

Point toward 12 months when:

- Income has increased meaningfully in the past year

- The borrower has less than two years of self-employment history

- A prior year was anomalous due to a business disruption

- The purchase timeline is compressed and documentation speed matters

- The borrower’s current performance significantly outpaces their 24-month average

Point toward 24 months when:

- Income is consistent and well-established over multiple years

- The prior year was stronger than the current year

- The borrower needs stronger income consistency to meet DTI requirements

- Complex income sources benefit from a fuller picture

- The borrower’s 24-month average produces better qualifying income than their 12-month

In either case, consider:

- Total account types available (personal, business, or both)

- Whether W-2 income can be blended to strengthen the qualification

- What expense ratios are likely to apply given the borrower’s industry

- LTV requirements relative to the borrower’s available down payment

- Reserve levels and compensating factors

How to Position This with Self-Employed Clients

One of the most valuable things you can do as a broker working in the Non-QM space is help self-employed clients understand that their tax strategy didn’t disqualify them from homeownership—it just means they need a lender who knows how to read their actual financial picture.

The conversation tends to go better when you lead with the logic: bank statement loans exist because the tax code and the mortgage system weren’t designed by the same people. Your clients didn’t do anything wrong. They did exactly what their accountant advised. And there are programs built specifically for people in their situation.

That framing removes the shame some self-employed borrowers carry when traditional lenders turn them away, and it positions you as someone who understands their world rather than someone trying to fit them into a box that was never designed for them.

From there, the 12-versus-24-month question becomes a practical conversation about which window tells their best story—not an obstacle, but a choice.

Bank Statement Loans as a Business Development Tool

Every self-employed borrower who couldn’t get financing elsewhere and found a path through you is a referral source for the next ten. Small business communities talk. Realtors who specialize in working with entrepreneurs and business owners talk. Once you develop a reputation as the broker who can get deals done for self-employed clients, that segment tends to grow organically.

Bank statement loans are also a natural entry point into a deeper Non-QM conversation. The business owner you helped purchase a home using bank statement documentation is often also an investor with properties they’d like to expand—or a candidate for DSCR financing on their first rental. The self-employed borrower who’s asset-rich may eventually be a fit for an asset qualifier program as well.

Building Non-QM fluency starts somewhere. For many brokers, bank statement loans are the most intuitive entry point because the borrower profile is so familiar and the problem being solved is so clear. Start there, and the rest of the product suite tends to follow naturally.

Common Broker Questions About Bank Statement Scenarios

What if my borrower has both personal and business accounts with significant intermingling?

Commingled accounts require more documentation, but they’re not automatically disqualifying. Underwriters will typically need a letter of explanation from the borrower describing how the account is used, along with any supporting documentation—a business license, CPA letter, or entity formation documents—that helps establish which deposits are business income versus personal transfers. The key is helping borrowers organize their statements before submission so the income sources are easy to trace. Your Account Executive can walk through a specific commingling situation before you submit and flag any documentation gaps early. Reach out here to talk through your scenario.

What if my client uses multiple business entities?

We can combine statements from multiple business accounts to build a complete income picture—and we don’t require the borrower to be a 100% owner of each entity, which matters for serial entrepreneurs or investors with minority stakes across several LLCs. Each entity’s accounts can be aggregated, though each business will need to be verified separately. If your borrower structures different revenue streams through different entities, bring us the full picture and we’ll work through how to document each one.

Can a borrower switch from 24-month to 12-month mid-process if the numbers work better?

Generally, yes—but timing matters. The cleaner window to make the switch is before the income calculation is finalized by underwriting, ideally before conditional approval. Once an income figure has been issued, changing the documentation window requires re-review and can introduce delays. This is the practical reason to run both scenarios before submission: a quick side-by-side calculation upfront takes minutes and can prevent a mid-process pivot that costs your client a week. Your Account Executive can run both income calculations for you before you formally submit.

How long does a borrower need to have been self-employed to qualify?

Generally, we look for a minimum of two years of self-employment history—but this isn’t a hard cutoff in every scenario. What underwriters are really evaluating is whether the income is stable and likely to continue. A borrower with 18 to 24 months of consistent deposits in a clearly established business, supported by a business license and CPA letter confirming the nature and duration of operations, can often be a workable scenario. The shorter the history, the more the surrounding documentation needs to do. Strong compensating factors—credit score, reserves, LTV—carry more weight when employment history is on the shorter end. Bring us the scenario and we’ll tell you where it lands. Talk to your Account Executive here.

Can bank statement loans be used for investment properties, not just primary residences?

Yes. Our bank statement program is available for primary residences, second homes, and investment properties, which makes it a versatile tool for self-employed borrowers who are also building a real estate portfolio. That said, if your client is purchasing an investment property and wants to qualify on the rental income from the property itself rather than their personal income, a DSCR loan may be a cleaner fit—no personal income documentation required at all. Many of our broker partners use bank statement and DSCR programs side by side depending on which tells the stronger story for a given deal.

How do bank statement loans handle business expenses for sole proprietors versus S-corp owners?

The income calculation works differently depending on business structure, and understanding the distinction helps you set accurate expectations with clients before submission.

For sole proprietors, we analyze gross deposits from personal or business accounts, then apply the expense factor from the Self-Employment Questionnaire to arrive at qualifying income. Because sole proprietor finances often flow through a single account, consistent monthly deposits are especially important here.

For S-corp owners, the picture is typically split: the borrower receives W-2 distributions from the business alongside any additional deposits from business accounts. We can blend both income streams—W-2 income combined with bank statement income—to build the strongest qualifying number. The business accounts and the W-2 are treated as complementary rather than competing documentation.

If your client’s business structure is more complex—multiple entities, mixed ownership, or distributions across both personal and business accounts—contact your Account Executive before submission and we’ll map out the right documentation approach together.

Working With Us on Bank Statement Scenarios

We accept bank statement loan scenarios at any stage—you don’t need formal approval to discuss a deal. Our Account Executives are available to work through documentation questions, run income calculations, and help you identify whether a 12-month or 24-month option better serves your client before you submit. Pre-qualifications are typically returned within 24 hours, which matters when your clients are working against purchase contract timelines or competing in active markets.

Self-employed clients deserve a lender who understands how they actually earn money. When you bring us those scenarios, we’ll do the work with you.

Explore our Bank Statement Loan program or contact your Account Executive to discuss a specific scenario.