Help your real estate investor clients scale their 1-10 unit properties portfolios—without personal income ever entering the equation.

DSCR “Ease of Use”

- The Ratio is Your Income: No additional income documentation required.

- Simplified Documentation: Only a completed Schedule of Real Estate Owned (SREO) is needed.

- No External Ratings: Mortgage ratings on other properties are not required.

- Limited Verification: No need to verify taxes and insurance on other properties.

- Investor-Friendly: Close multiple loans for the same investor simultaneously.

- Efficient Execution: Fast closings with minimal conditions.

THE OPPORTUNITY

The Gap in Your Product Menu Is Costing You Deals

DSCR is a common offering. A seamless, investor-ready DSCR experience is not. Your clients are looking for a close that happens without headaches, conditions that make sense, and a lender who understands how portfolio investors operate.

That’s what we bring to the table. From scenario submission through funding, we keep the process straightforward so you can focus on building the relationships that drive your business forward.

Our DSCR program is designed to support investors seamlessly at every stage of portfolio growth, and to make you the broker who helped them get there.

HOW A DSCR LOAN WORKS

Property Cash Flow Is the Qualification. That’s It.

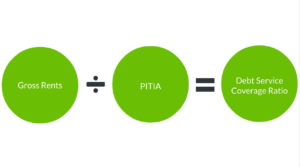

DSCR stands for Debt Service Coverage Ratio. It’s straightforward:

DSCR = Gross Rent Lease or Form 1007/216 divided by PITIA

DSCR > 1.0 means there is sufficient cash flow to cover the debt service

DSCR < 1.0 means there is not enough cash flow to cover the debt service

Rent is determined by the appraiser’s Form 1007 rent schedule—a professional estimate of what the property will rent for at market. We also accept AirDNA® data for short-term rental analysis when working with Airbnb or VRBO properties.

What we look at:

- The property’s rental income (Form 1007)

- Borrower’s credit score

- Borrower’s liquid assets

What we don’t look at:

- W-2 income

- Tax returns

- Personal DTI

- How many other mortgages your borrower already has

Each loan stands on the strength of that one property’s cash flow.

PROGRAM SPECS

DSCR Program Details

1–4 Unit Properties

- Loan Amounts as High as $3,000,000

- Cash-Out Available Up to $500,000

- Purchase LTV Up to 85%

- Rate & Term LTV Up to 80%

- Cash-Out Refinance LTV Up to 75%

- Credit Score as low as 660

- DSCR Ratio as Low as 0.75 (no-ratio options also available)

- 30-year fixed or 40-year interest-only (10-year IO + 30-year fixed amortization)

- SFR, condos, non-warrantable condos, short-term rentals

5–10 Unit Properties

- Loan Amounts as High as $3,000,000

- Cash-Out Available Up to $500,000

- Purchase LTV Up to 75%

- Rate & Term LTV Up to 70%

- Cash-Out Refinance LTV Up to 65%

- Credit Score as Low As 680

- DSCR Ratio as low as 1.1x

- 30-year fixed or interest-only options

- Must close in LLC; experienced investors only; maximum 2 vacant units at closing

Maximize Monthly Cash Flow with LendSure’s 10/40 Fixed-Rate Interest Only

Why choose LendSure’s 10/40 Fixed-Rate Interest-Only loan? Because it offers the ultimate edge in a competitive market. Savvy investors use this program to maximize monthly cash flow and boost purchasing power, all while securing a 40-year fixed rate. This innovative solution provides the flexibility to make lower interest-only payments or switch to fully amortized payments at any time, with zero penalties.

Built to Scale—and Built for Brokers

Close Multiple Loans in One Transaction Your investor client is buying two properties at once? Refinancing one while acquiring another? We can close multiple DSCR loans for the same borrower in a single transaction. Most lenders require separate closings. We don’t. That’s fewer headaches for you and faster momentum for your client.

No Documentation on the Rest of the Portfolio As your clients grow their portfolios, traditional lenders start requiring documentation on every property they own. With DSCR, we’re only looking at the property being financed. Other mortgages just need to show “paid as agreed” on the credit report. That’s it.

Interest-Only Qualification Option Our 40-year interest-only program qualifies borrowers on the IO payment for the first 10 years, then fully amortizes over 30 years. Lower payments mean better DSCR ratios and an easier path to approval—especially in higher-rate environments.

Short-Term Rental and Specialty Properties Vacation rentals, condotels, non-warrantable condos—we finance them. We work with appraisers experienced in STR valuations and accept AirDNA® reports for rental income analysis. An 80% multiplier is applied to gross short-term rental income for qualification purposes.

Foreign Nationals and Non-Traditional Borrowers Welcome U.S. citizenship is not required. We lend to foreign nationals and non-permanent residents who are investing in U.S. real estate. If your client has the cash flow, we’ll look at the deal.

24-Hour Term Sheets. 15–20 Business Day Closings. No income verification means fewer conditions and faster underwriting. Submit a scenario and you’ll have preliminary pricing and a term sheet within 24 hours. Average time from application to funding is 15–20 business days.

Cryptocurrency Accepted for Reserves A differentiator worth knowing: we accept cryptocurrency as eligible reserves. For crypto-forward investors, this removes a documentation barrier that stops deals at other lenders.

DSCR vs. Traditional Investment Lending

| Feature | Traditional Loans | LendSure DSCR |

| Income Documentation Required | Yes | No |

| Tax Returns Required | Yes | No |

| DTI Limits Portfolio Size | Yes | No |

| Multiple Loans in One Closing | No | Yes |

| Interest-Only Options | Limited | Yes (40-year available) |

| Non-Warrantable Condos | Rarely | Yes (up to 75% LTV) |

| Condotels / Short-Term Rentals | Rarely | Yes |

| Minimum DSCR Ratio | 1.25 typically | 0.75 |

| Average Closing Time | 30–45 days | 15–20 days |

| Portfolio Scaling Potential | Limited by DTI | Unlimited by cash flow |

Now’s the time to get started.

Have a question? We have the answers.

How is DSCR calculated?

A simple way to calculate your DSCR and measure your cash flow is to divide the monthly rent by the PITIA (principal, taxes, interest, insurance, and association dues). The resulting ratio lends insight into your ability to pay back the loan based on your property’s monthly rental income.

DSCR = Gross Rent Lease or Form 1007/216 divided by PITIA

DSCR > 1.0 means there is sufficient cash flow to cover the debt service

DSCR < 1.0 means there is not enough cash flow to cover the debt service

Does my borrower need to provide tax returns or income documentation?

No. We don’t require W-2s, tax returns, pay stubs, or personal income verification. Qualification is based on property cash flow. Your borrower will provide a credit report and asset documentation, but personal income is not part of the equation.

How many properties can my borrower finance with DSCR?

There’s no portfolio limit. Each property is evaluated independently on its own cash flow. As long as each one qualifies on its own, your borrower can keep scaling.

Can we close multiple DSCR loans for the same borrower at the same time?

Yes. We can close multiple loans in a single transaction—whether your borrower is purchasing two properties simultaneously or refinancing one while acquiring another.

What property types are eligible?

Single-family homes, multifamily up to 10 units, condos, non-warrantable condos, condotels, and short-term rentals. If it has verifiable rental income, bring us the scenario.

How do you handle short-term rental income?

We accept AirDNA® reports and 12-month Airbnb/VRBO earning summaries. We apply an 80% multiplier to gross short-term rental income for qualification, and we work with appraisers who specialize in STR valuations. Always request both long-term and short-term rent notations on the appraisal.

What if DSCR doesn’t work for my borrower’s scenario?

Submit the scenario anyway and we’ll help you find the right path. Bank statement loans, hybrid income approaches, or a full-doc loan may be a better fit. We credit 100% of rental income under the bank statement program and handle negative cash flow as an income reduction—not a liability—which can make a meaningful difference.

Does my borrower need to be a U.S. citizen?

No. We lend to foreign nationals and non-permanent residents. Bring us the scenario.

How quickly can we close?

We issue 24-hour term sheets. Average time from application to funding is 15–20 business days. Because there’s no income verification, there are fewer conditions to clear—which means fewer delays.

Have a Scenario? Let’s Look at It.

Click here to submit your loan scenario or call us today at (888) 707-7811.

Investment property clients are some of the most motivated borrowers in the market—and they’re often being turned away by lenders who don’t have the right product. If you have a borrower who owns rental properties, is building a portfolio, or has run into a DTI wall with a conventional lender, we want to hear about it.

Resources

May 28, 2025

A Broker’s Guide to LendSure’s DSCR Loan Program

You’re working with a real estate investor who’s ready to expand their portfolio. The …

Read More

October 23, 2024

Why You Should Offer DSCR Loans

As the real estate market continues to shift, investors are looking for new ways to expand…

Read More

May 15, 2024

The Complete Guide To DSCR Rental Property Loans

Designed for property investors, a debt service coverage ratio (DSCR) is a way to finance …

Read More

November 8, 2023

3 Reasons to Tap Into the Non-QM DSCR Market in 2023

It’s no secret – the real estate market has slowed over the last few months. With high…

Read More

August 30, 2023

Full Doc Loans vs. DSCR Loans: What’s the Difference?

When it comes to financing properties, your clients have a wide range of options to choose…

Read More

July 26, 2023

In an uncertain market, DSCR program can keep your pipeline full

The housing market has been slowing since 2022, but the shortage of housing hasn’t gone …

Read More

March 22, 2023

Investment properties with DSCR - Non-QM 101

The U.S. housing market has been a profitable one for landlords in recent years. Generally…

Read More

November 9, 2022

DSCR - A LendSure Program Built for Investors

The housing market has slowed in recent months, and values of single and multifamily prope…

Read More

April 20, 2023

Loan Scenario: Investor Cash Flow (DSCR)

Loan Scenario: Investor Cash Flow (DSCR) LendSure's Investor Cash Flow (DSCR) uses the pro…

Read More